Vol Lower, But Vol Of Vol Higher Last Week Plus SVIX Weeklys Now Available

Saturday Review For November 25, 2023

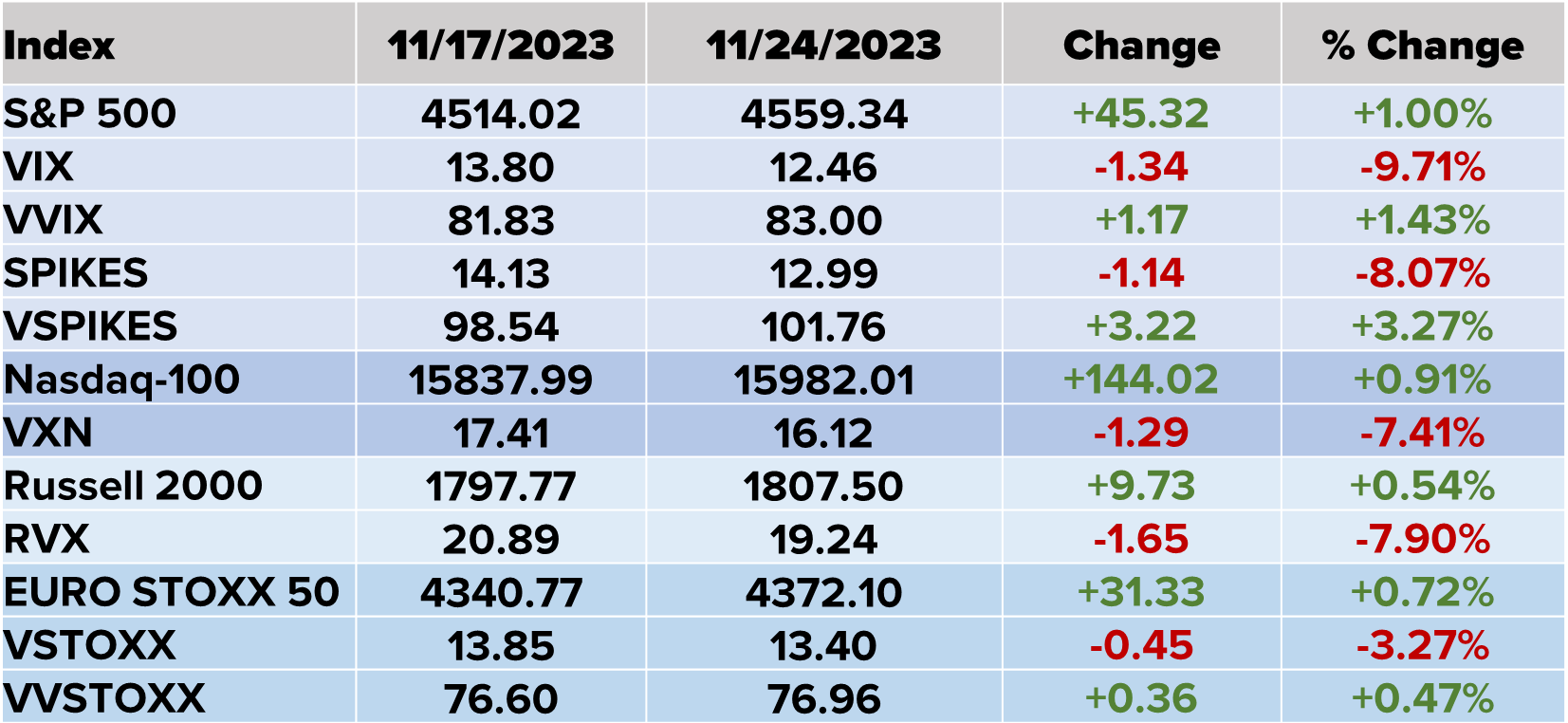

The S&P 500 (SPX) led the markets higher last week gaining exactly 1.00% while the Nasdaq-100 (NDX) and Russell 2000 (RUT) we higher by less than 1%. For the second week the red and green is mixed on the table below as VVIX and VVSTOXX where higher while VIX and VSTOXX lost value. This is not uncommon in the volatility space. Both VIX and VSTOXX are range bound measures so where they are at the low end of the range, we see call buyers come into the market, pushing implied volatility higher. Finally, we noted RVX rising last week as RUT moved up as well. This is attributed to call buyers, which is unusual for volatility indices based on a broad market index. The lack of continued upside in RUT, after rising over 5% the previous week, resulted in RVX dropping almost 8%.

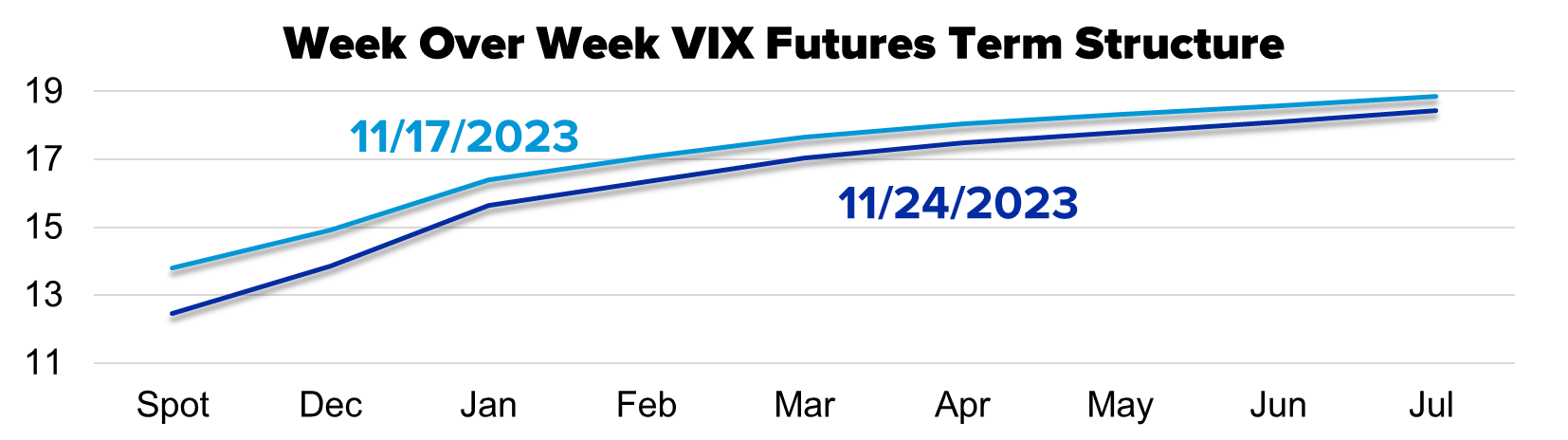

VIX moved lower, in combination with SPX higher, but also note December is a tough month for upside in VIX due to a few extra holidays relative to other times of the year. VIX at 12.46 is a 52-week low and likely too low according to many market observers. Pay close attention to the second month (January) contract over the next few weeks as it may start to give us hints around the mind of the market for early 2024.

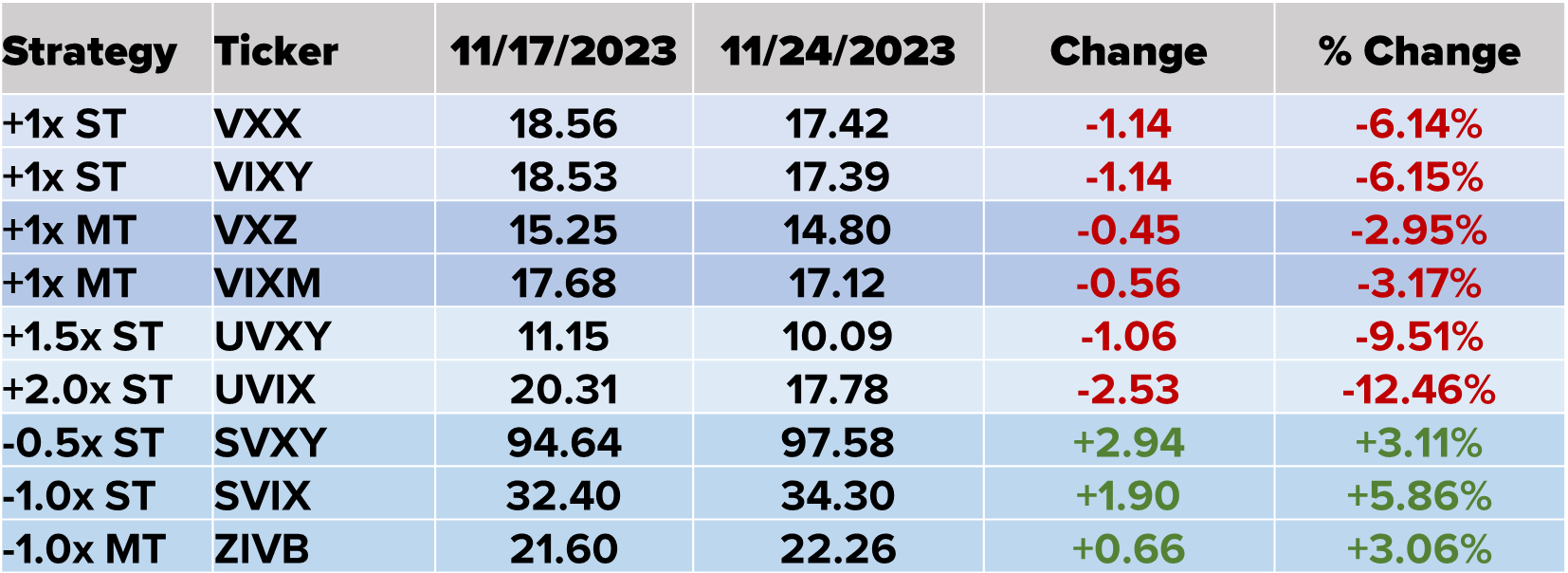

We usually do not have too much to talk about around the performance of the volatility related ETPs as SVIX is the big winner when VIX is lower and UVIX tends to lead the pack when VIX is higher. However, the table below shrunk by two funds last week as the two funds based on the SPIKES index were liquidated. We know the volume was not great, but competition is always good for markets and the loss of SPIKES as an alternative to VIX is disappointing.

We did get something new last week as weekly expirations are now available for SVIX. It is no secret that SVIX is our favorite volatility related ETP, and we sell calls periodically against our long position. However, the first sizable trade using weekly SVIX options appears to be a put sale. On Wednesday last week, less than an hour into the trading day, someone sold 100 of the SVIX Dec 33 Puts for 0.85. This trade went off with SVIX at 33.15. A short put results in the obligation to purchase the underlying at the strike price, which would result in an effective cost of 32.15 (33.00 – 0.85) if SVIX closes under 33.00 this coming Friday.

European volatility, as measured by VSTOXX, was lower and the futures followed the index down. Unliked VIX, VSTOXX is slightly higher than the 52-week low of 12.89 from June this year.

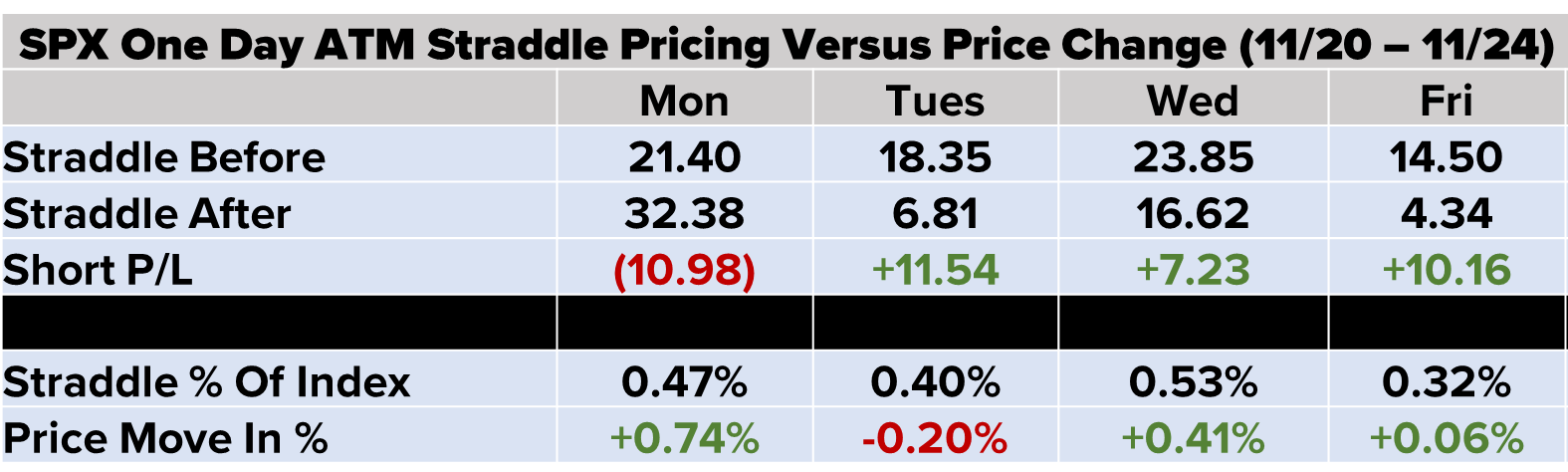

We are expanding the markets with daily option expirations to include the DAX, which just completed the first full week of daily expirations. Before getting to that, SPX volatility sellers missed the mark on Monday, but made up for it over the balance of the week. On Monday, SPX rose 0.74% while the straddle priced in a move of 0.47%. The other three expirations last week priced in lower-than-average daily price change for 2023 of +/-0.67%, but still overpriced the following day’s move.

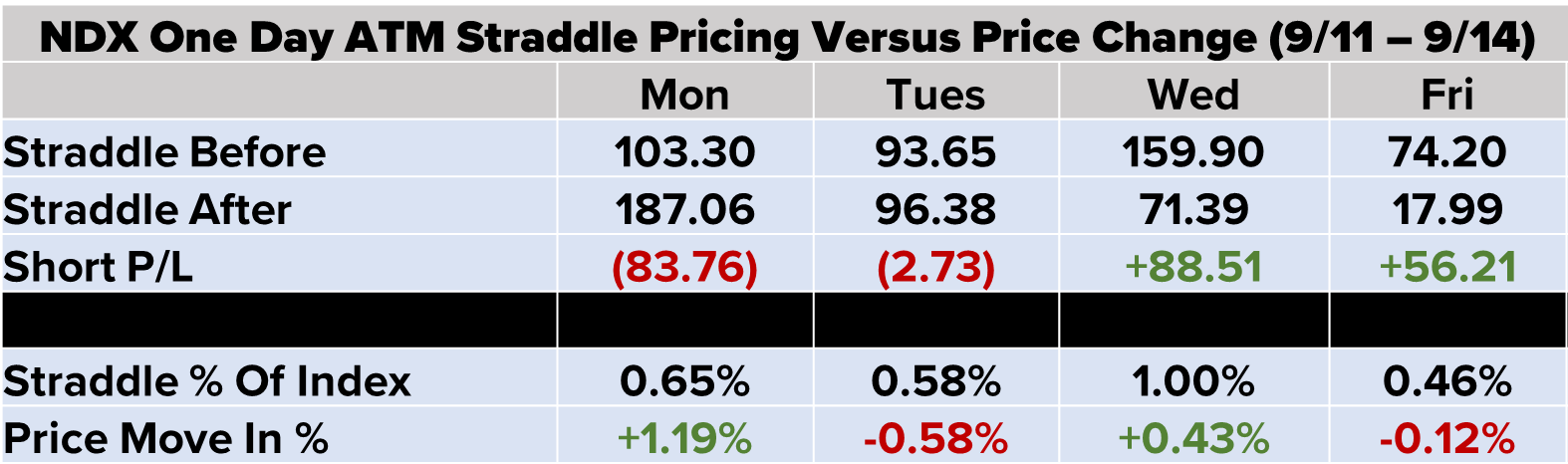

NDX straddles underpriced Monday and Tuesday expirations and then overpriced both Wednesday and Friday. Note the elevated straddle pricing on Wednesday. The first thought is traders bid up NDX option prices after two consecutive instances of underpricing. However, this relates to NVIDA (NVDA) reporting earnings after the close on Tuesday with the subsequent price impact on Wednesday. NVDIA earnings resulted in the stock dropping about 2.5%, much lower than the average price change or around +/-6.5%. NVDA is over 4% of the composition of NDX. The anticipation of a bigger move out of NVDA pushed NDX price higher.

European option sellers did very well last week as both the EURO STOXX 50 and DAX 1-day straddles overpriced the subsequent market change all five days last week. The average price change for the EURO STOXX 50 in 2023 is +/-0.68%. No straddle was priced higher than this level nor did any day last week see a price change that came close to that level.

As noted, DAX is relatively new, but liquidity is already facilitating block trades (last week’s Saturday review discussed the first block treading using daily DAX options). The average DAX daily price change in 2023 is +/-0.63%. All five straddles priced lower moves than this average and the price changes were all much lower than the average move resulting in a good week for option sellers.