Saturday Review For June 10, 2023

Breaking Down A Large VIX Option Trade From Last Week

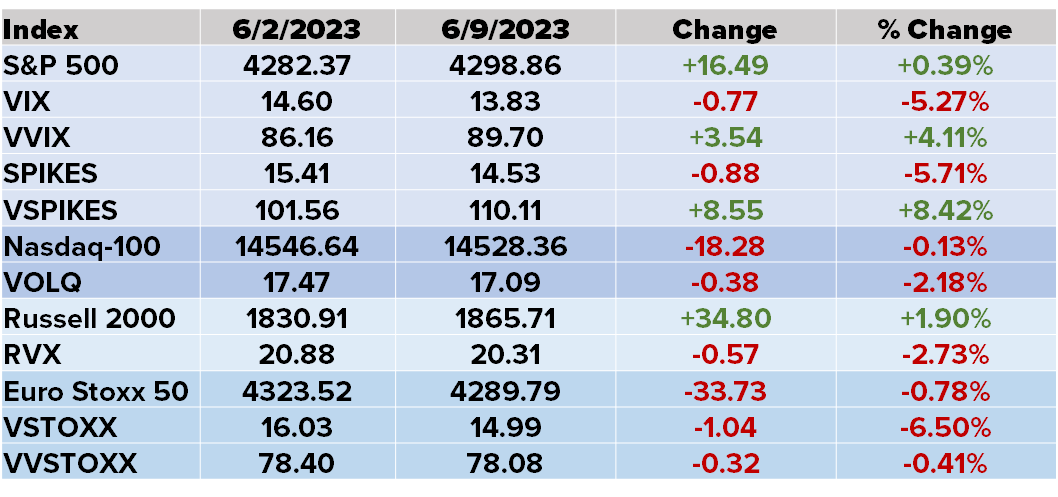

Last week was a mixed one for stocks with the Russell 2000 (RUT) gaining 1.90% and the S&P 500 (SPX) rising by 0.39%. The Nasdaq-100 (NDX) was lower by 0.13%, the first time NDX lost value when the SPX gained since September 2021. NDX has been a leader in 2023, but seems to be fading a bit. VIX managed to finish the week with a 13 handle, something that is pretty normal, but not a level we have seen since before the early days of the Covid pandemic.

We manually put this table together as it gives us more of a ‘feel’ for the week over week market changes than just downloading the data. I share this as we were a bit surprised at the outperformance of the Russell 2000 (RUT) versus the S&P 500 (SPX) and Nasdaq-100 (NDX) last week. This is likely due to our short-term memory recalling RUT under pressure at the end of the week, but not recalling how strong the small cap benchmark was to start the week. We put together a chart, indexing each major US index to 100 to get a side-by-side comparison of individual index performance last week.

Note at one-point last week, RUT was outperforming NDX by almost 5%. However, that gap narrowed over the course of the last two days of the week.

The VIX curve continues to drift lower in a parallel fashion. However, the spread between the front month June contract and spot VIX has narrowed. We were surprised as next week brings an FOMC announcement which we felt would provide expected volatility a slight boost.

The volatility related ETPs acted as expected. The long funds lost value with UVIX dropping almost 18%. The best performing funds was SVIX, which offers short volatility exposure, which gained 9.4%. We also want to highlight ZIVB, which offers short exposure farther out on the VIX curve, which was up over 5%. ZIVB is relatively new, having launched in mid-April. Despite the short life, ZIVB is up about 16.5% since launch.

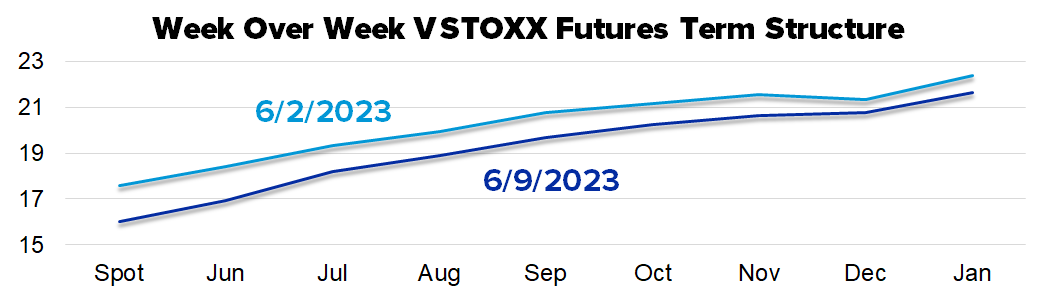

The VSTOXX curve reflected the performance of the VIX curve shifting lower across all contracts. VSTOXX has been at a discount to VIX as the debt ceiling debacle loomed over the US markets, but it is now at a premium relative to VIX.

On Thursday, vol traders received an overdue piece of news as the ProShares Ultra VIX Short Term Futures ETF (UVXY) announced a 1 for 10 reverse split which is effective June 23. We say overdue as UVXY was trading in the single digits for a while which often leads to a reverse split. Options outstanding on UVYX will become non-standard options and when this happens, we usually see an evaporation of liquidity. Something to keep in mind when considering a new position over the next couple of weeks. This appears to be the eleventh split since UVXY was launched in 2011. The full history shows up below.

Finally, just for fun, we did some math. The split adjusted closing price on the first day of trading for UVXY (October 3, 2011) was about $2,058,000,000.

Finally, there was a large VIX trade that got some mainstream attention last week. On Thursday, with the July VIX future at 17.43 and spot VIX at 14.10 a trader purchased over 80,000 VIX Jul 23 Calls for 0.87. Over the course of Thursday another 20,000 or so traded at similar prices. Then on Friday about 50,000 more of these calls were purchased for 0.92.

The popular press presented this as a trader betting on a 60% rise in VIX, which appears to be based on the strike price (23.00) versus where VIX was when the trade was executed (14.10). However, those that understand the VIX derivative marketplace know that a trade like this usually needs to be monetized (think take profits) when VIX moves higher. We created the following payoff diagram showing the profit and loss for this trade each Friday between trade date and standard July VIX expiration.

The pricing for the underlying is the July VIX future, not spot VIX as VIX options share pricing assumptions with the corresponding futures. Note the break-even for all, expect the final date above, is well below the strike price of 23.00.

For a final look at this trade, we calculated the approximate July VIX future price to achieve profits of 0.89, 1.78, and 2.67. These are not arbitrary numbers as they represent 1x, 2x, and 3x profits relative to the average cost of 0.89.

If July VIX climbs to 20.70 this coming Friday, the trader may have a chance at taking a 100% profit and moving on to the other trade. At 24.10, likely requiring a dramatic down day or two for stocks, the trade profit would be 2.67. The closer we get to July expiration, the higher the levels to achieve these profit levels.