Historical Index And Option Price Action Around CPI (Tuesday) And FOMC (Wednesday)

Sunday Preview For Week Of December 11 - 15

There are two big announcements on the docket next week, Tuesday before the market opens, we get the Consumer Price Index (CPI) readings for November. Then Wednesday afternoon we get the last FOMC announcement for 2023.

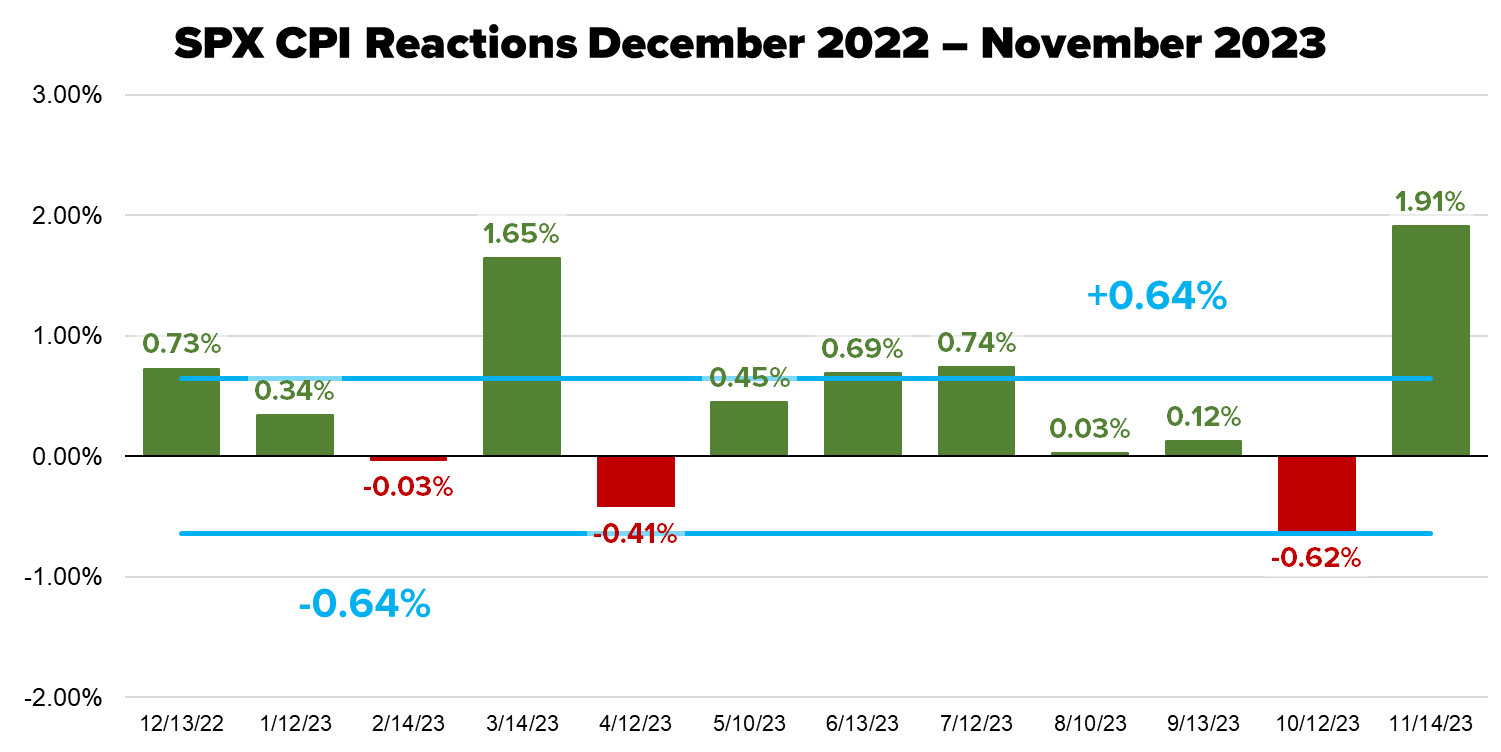

The average price change over the last twelve CPI announcements has been +/- for the S&P 500 (SPX). Last month, traders were lulled into a sense of security as the price change on CPI Day had not exceeded 1% since March this year. Note the average move on CPI Day is +/-0.64% while the average day for SPX over the same period is a move of +/-1.07%.

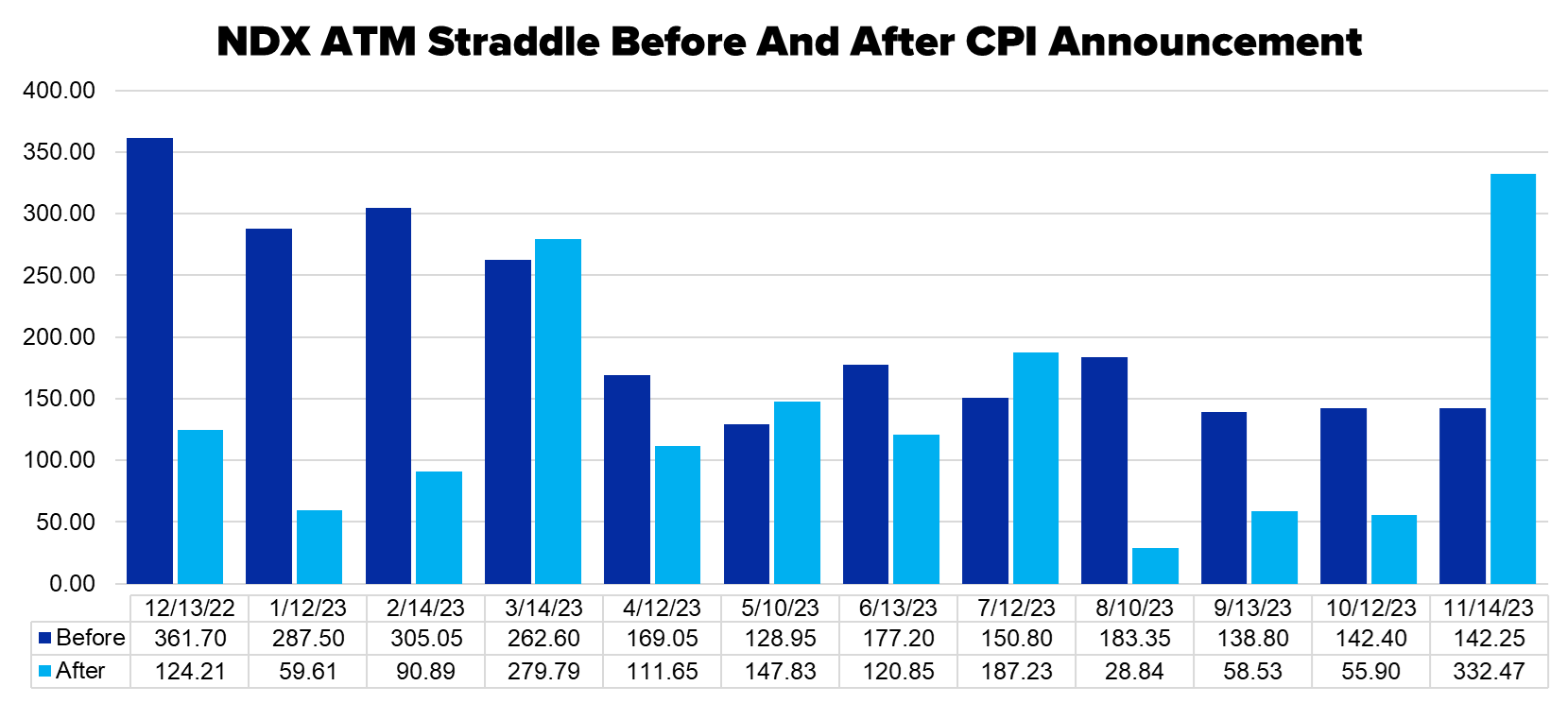

The second chart related to SPX on CPI days shows the 1-day at-the-money (ATM) straddle price the day before and at expiration on announcement date. The lower dark blue bars on the right side of the graphic show much lower anticipated price action around SPX on CPI Day. However, after the almost 2% move last month, we may see some elevated option premiums.

As expected, the pattern of Nasdaq-100 on CPI Day is like that of SPX, but the moves are more accentuated. The average move is +/-0.98% on announcement dates which is exceeded by the average daily move of +/-1.34% on all trading days over the same period.

A seller of the NDX Nov 14th ATM straddle the evening before the announcement could have taken in 142.25 and the straddle’s value on the close was almost 190 points higher at 332.47. This sort of underpricing can influence premiums for the next announcement.

Daily option expirations are relatively new to the EURO STOXX 50 (SX5E) and DAX indices. Both close mid-morning US time and do react to major US economic numbers. However, as daily SX5E options were launched in late August and DAX daily options are just a few weeks old, we only have price change data on CPI Day to work with.

The average price change for SX5E on days when CPI is released is +/-0.89%. This figure is an interesting contrast to the numbers for SPX (average CPI change +/-0.64%) as both have approximately the same volatility over long periods of time and the respective volatility indices (VSTOXX and VIX) are usually within the same range. However, not only is the SX5E average CPI price change higher than SPX, but it is also higher than the average SX5E day of +/-0.69%.

Finally, DAX reflects the comments above about SX5E as the average price change on CPI Day is +/-0.86%, higher than SPX, but also higher than the average price change over all days of +/-0.64%. We are looking forward to this time next year when we have more data to work with and can discuss the straddle pricing for both SX5E and DAX.

Of course, all eyes will be on the FOMC announcement this coming Wednesday. The market is focused on when the first rate cut will occur, with the current odds pointing to the May 1, 2024 meeting. A week ago, the outlook was for a cut at the March 20, 2024, meeting. However, after this past Friday’s employment report the odds of a cut in March dropped to 44.5% (from over 60% earlier in the week). We will be watching what the market reaction is to the announcement, with a keen eye on the March odds with an increase likely bullish for stocks and a decrease in the chance of a cut in March bearish for stocks.

Unlike CPI reactions, the SPX average change on the last twelve FOMC announcements is +/-1.20%. This figure covers announcements going back to June 2022. The average daily price change over this period for SPX is +/-0.84%, so FOMC day has been more volatile than the average trading day.

The last two straddles on FOMC day underpriced the following day’s SPX move. That factor combined with the uncertainty about the timing of the next FOMC rate change may result in elevated option premiums Tuesday afternoon.

The average FOMC day price change for NDX is +/-1.77%, much higher than the average daily price change over the same period of +/-1.13%. The last change was inline with the average move with a gain of 1.77% with a 1.46% drop on the previous report.

Straddle sellers got hit on the last two FOMC announcements, so like SPX we think options may be expensive, but keep in mind sometimes options are justifiably expensive. Stated a bit more plainly, if option premiums are elevated compared to the last two announcements, that does not automatically represent an option selling opportunity.